Hotel classification is one of the most strategically important and frequently misunderstood elements of hotel development. While many interpret hotel classification as simply a star rating, in reality, it determines the operational model, capital expenditure, staffing intensity, ADR positioning, regulatory compliance, and ultimately the asset’s exit value. For hotel owners and developers, hotel classification is not a branding exercise; it is a capital structuring decision that affects the entire lifecycle of the property.

A successful hotel classification aligns market demand, regulatory standards, cost per key, and return expectations. When misaligned, classification can lead to overcapitalisation, inflated payroll structures, or a product that does not meet investor yield thresholds.

Foundations of Hotel Classification

Hotel classification forms the conceptual backbone of hotel development strategy. Before examining regulatory systems, segmentation models, or valuation implications, it is essential to understand what hotel classification truly represents and how it has evolved. This section establishes the intellectual foundations of hotel classification, clarifying the distinctions among product, service, and market positioning, and tracing the historical development of star systems and commercial segmentation. Without this grounding, classification risks being reduced to a superficial label rather than a strategic framework.

What Is Hotel Classification?

Hotel classification is the structured categorisation of a hotel according to defined criteria relating to physical product, service provision, facilities, and positioning within a target market segment. The term encompasses both formal regulatory star ratings and commercial market segmentation, such as luxury, upscale, midscale, or economy.

From a development perspective, hotel classification operates across five interdependent dimensions: quality level, service level, market segment, property configuration, and regulatory framework. These dimensions collectively determine the asset’s feasibility model, cost benchmarks, and long-term operating performance.

The Historical Evolution of Hotel Classification

Hotel classification did not begin as a globalised star-rating system. Early forms of classification emerged in Europe in the early 20th century as a means of providing travellers with a simple indicator of comfort and service level. These systems were largely consumer-oriented, developed by automobile associations, tourism boards, and industry bodies to help standardise expectations in an increasingly mobile society.

Over time, star ratings became formalised within national regulatory frameworks. Governments adopted prescriptive criteria covering room size, facilities, and service standards, using classification as both a quality-control tool and a tourism marketing instrument. In many markets, classification was also linked to licensing and eligibility for international tour operators.

However, from the 1990s onward, the rapid expansion of global hotel brands began to shift the centre of gravity away from purely regulatory classification. Brand segmentation: luxury, upper upscale, upscale, midscale, economy, increasingly defined guest expectations, and more than national star systems. A globally recognised brand often becomes more meaningful than a domestic star rating.

The digital era further accelerated this evolution. Online review platforms and OTA ranking algorithms introduced a market-driven reputational layer that operates alongside, and sometimes supersedes, official classification. Today, hotel classification exists within a hybrid ecosystem of regulatory standards, brand positioning, and digital perception.

Understanding this evolution is essential. It explains why star ratings remain important, yet are no longer the sole determinant of market positioning or asset value.

Understanding Quality: Product Quality vs Service Quality

In hotel classification, the word “quality” is often used generically. However, it is critical to distinguish between product quality and service quality, as they are not the same, and regulatory systems frequently focus on one more than the other.

Product quality refers to the physical and tangible aspects of the hotel. This includes room size, bed specification, bathroom finish, building materials, soundproofing, public areas, meeting space, spa facilities, and FF&E standards. Product quality directly affects development cost per key and lifecycle capital expenditure.

Service quality refers to the human and operational delivery of the guest experience. It includes staff-to-room ratios, concierge capability, response times, housekeeping frequency, food and beverage execution, and overall guest engagement. Service quality significantly impacts payroll intensity and GOP margins.

A hotel may achieve high product quality but moderate service quality (for example, a design-led select-service hotel), or vice versa. Effective hotel classification requires clarity on which quality dimension drives the positioning strategy and financial model.

Star Ratings and Market Positioning

The most visible form of hotel classification is the star rating system. Although widely recognised, star ratings vary significantly from country to country in methodology and threshold requirements. In principle, higher star classifications imply higher product standards, broader facilities, and more extensive service provision.

| Classification | Typical Cost Impact | Operational Impact | Revenue Potential |

|---|---|---|---|

| 2–3 Star | Lower FF&E & public space requirements | Lean staffing | Moderate ADR, volume-driven |

| 4 Star | Higher finish standards, multiple outlets | Structured service model | Strong ADR in urban markets |

| 5 Star / Luxury | Premium materials, extensive amenities | High labour intensity | High ADR, lower occupancy tolerance |

However, it is essential for investors to understand that star ratings do not always equate to consistent international standards. A five-star hotel classification in one country may differ materially from that in another, particularly in room-size requirements and staffing expectations.

Although systems vary by country, star classifications generally reflect:

- Physical standards (room size, finishes, bathrooms, amenities)

- Public areas (lobby scale, F&B outlets, meeting rooms, spa facilities)

- Service level (concierge, 24-hour reception, valet, room service)

- Staff-to-room ratios

From a development standpoint, increasing hotel classification typically increases capex per key and labour intensity. The question for developers is not how many stars can be achieved, but whether the market supports the service level implied by the classification.

Regulatory and Regional Classification Systems

Hotel classification operates within diverse regulatory environments that vary significantly by country and region. While star ratings appear broadly comparable across markets, the underlying criteria, enforcement mechanisms, and spatial thresholds often differ materially. This section examines how hotel classification systems function across jurisdictions, including European harmonisation efforts and national frameworks, and explores the implications of prescriptive standards, fragmentation, and emerging-market star inflation for developers and investors.

Regional Variation in Hotel Classification

Hotel classification systems vary enormously across regions and countries. Regulatory classification may be government-controlled, industry-led, voluntary, or mandatory. Standards differ in their focus on room size, bathroom configuration, facility provision, and service availability.

In Europe, many countries follow structured classification frameworks, but these are not fully harmonised. Some examples include:

Selected European Hotel Classification Frameworks

| Country | Classification Authority | System Type | Key Characteristics |

|---|---|---|---|

| Austria | Hotelstars Union | Harmonised EU system | Structured evaluation and periodic review |

| Bulgaria | Ministry of Tourism | National, mandatory | Regulatory compliance-driven classification |

| Czech Republic | Hotelstars Union | Harmonised EU system | Points-based criteria aligned with EU framework |

| France | Atout France | Government-regulated | Mandatory review cycle (typically every 5 years) |

| Germany | DEHOGA (Hotelstars Union) | Industry-led, voluntary | Widely adopted scoring-based system |

| Hungary | National Tourism Certification Board | National, aligned with EU standards | Structured, checklist-based criteria |

| Italy | Regional Authorities | Decentralised | Significant regional variation in standards |

| Netherlands | Hotelstars Union | Harmonised EU system | Standardised scoring methodology |

| Poland | Ministry of Sport and Tourism | National, mandatory | Formal star system with regulatory thresholds |

| Romania | Ministry of Economy, Entrepreneurship and Tourism | National, mandatory | Centrally regulated classification framework |

| Spain | Autonomous Communities | Decentralised | Criteria vary by autonomous region |

| Türkiye | Ministry of Culture and Tourism | National, mandatory | Points-based, prescriptive national system |

| United Kingdom | AA / VisitBritain | Voluntary | Inspection-based and market-influenced |

Hotelstars Union and European Harmonisation

The Hotelstars Union (HSU) is a pan-European initiative established in 2009 under the umbrella of HOTREC (Hotels, Restaurants & Cafés in Europe) to harmonise hotel classification standards across participating countries. Its objective is to create a comparable, transparent star-rating framework that reduces fragmentation across national systems. The Hotelstars Union applies a structured, points-based catalogue of criteria covering room size, facilities, service provision, safety, quality management, and increasingly sustainability. Hotels are assessed against a unified scoring matrix, and classification is typically valid for a defined period before reassessment. The aim is to improve consumer clarity while providing greater cross-border consistency for operators, investors, and developers.

As of today, the Hotelstars Union includes more than 20 European countries, among them Austria, Belgium, the Czech Republic, Denmark, Estonia, Germany, Greece, Hungary, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Slovakia, Slovenia, Sweden, and Switzerland (membership has expanded gradually over time). While the system significantly improves comparability within participating markets, it is not universal across Europe.

Major tourism markets such as France, Italy, Spain, Türkiye and the United Kingdom operate their own national or regional classification frameworks outside the HSU structure. Furthermore, even within the Hotelstars Union, interpretation and enforcement may vary across national levels. For developers and investors, this means that although the HSU represents an important step toward harmonisation, hotel classification across Europe remains only partially standardised.

Countries such as France and Türkiye operate centrally administered systems with mandatory compliance. Italy and Spain, by comparison, rely on regional authorities, creating internal variation within a single country.

For international investors and developers, this fragmentation means that hotel classification cannot be evaluated in isolation from location. A five-star hotel classification in one jurisdiction may represent a materially different product standard in another. Developers targeting global operators or institutional exit strategies frequently design to brand standards that exceed local regulatory minimums.

Prescriptive Standards and Investment Implications

A recurring theme across many regulatory hotel classification systems, in Western Europe, Southern Europe, and parts of Central and Eastern Europe, is the reliance on prescriptive criteria. These systems typically define required facilities and minimum room dimensions but do not necessarily mandate generous spatial planning, experiential quality, or contemporary design standards.

In practical terms, this means that regulatory hotel classification often represents a minimum compliance threshold rather than a definitive indicator of investment-grade product quality. In some markets, minimum room sizes for higher classifications may be relatively modest compared to international luxury benchmarks. As a result, regulatory classification may present low barriers to achieving higher star ratings.

For developers, this creates three important considerations:

- Regulatory classification should not be confused with market positioning.

- International brand standards frequently exceed national requirements.

- Feasibility modelling should be based on demand-driven ADR assumptions rather than star rating alone.

The Risk of Star Inflation in Emerging Markets

In certain emerging or rapidly developing tourism markets, the number of hotels classified at the highest star levels has increased significantly over short periods. This phenomenon, sometimes referred to as “star inflation”, occurs when regulatory systems permit relatively accessible pathways to higher classifications.

Star inflation can arise from several factors:

- Political incentives to promote high-end tourism

- Facility-based checklist systems with modest spatial thresholds

- Rapid expansion of supply in destination-led markets

- Limited differentiation between upper upscale and luxury criteria

When a large proportion of new supply enters a market as a five-star product, ADR compression often follows. The label remains, but pricing power erodes due to oversupply and lack of experiential differentiation.

For investors, star inflation creates two risks. First, the regulatory classification may overstate the asset’s true competitive positioning. Second, exit buyers may discount nominal star level in favour of brand strength, RevPAR index performance, and operational quality.

This reinforces a core principle of hotel classification: regulatory star level should never be treated as a proxy for value. Market positioning, brand alignment, and performance metrics ultimately determine asset resilience.

Cross-Border Development Considerations

When operating across multiple jurisdictions, whether in Western Europe, the Mediterranean, or Central and Eastern Europe, hotel classification must be integrated into feasibility analysis, brand selection, and exit strategy from the outset.

Developers should assess:

- Whether local classification standards align with target market expectations

- Whether brand requirements exceed regulatory minimums

- Whether spatial thresholds support intended ADR positioning

- Whether the classification level enhances liquidity at exit

Hotel classification, particularly in cross-border development, is therefore both a regulatory compliance issue and a strategic investment decision. Understanding regional variation, without assuming uniform standards, is essential to protecting long-term asset value.

Quantitative Comparison of Classification Standards

Understanding hotel classification requires moving beyond descriptive categories and into measurable criteria. Quantitative thresholds such as minimum room size, facility requirements, and service obligations materially influence capital expenditure, land efficiency, and operational intensity. This section introduces a comparative example of regulatory standards to illustrate how identical star ratings can represent substantially different development footprints and investment risk profiles.

Example Regulatory Minimum Room Size Comparison Türkiye vs. Abu Dhabi

To illustrate how regulatory hotel classification standards vary across jurisdictions, the table below compares minimum guest room size requirements for three-, four-, and five-star city hotels in Türkiye and Abu Dhabi.

Both systems operate under formal regulatory frameworks, yet their spatial thresholds differ materially. By focusing solely on minimum room size, one of the most fundamental classification criteria, the comparison shows that identical star ratings can reflect significantly different development intensities. This example highlights why hotel classification should not be interpreted as internationally equivalent without examining the underlying quantitative standards.

| Star Level | Türkiye – Minimum Room Size* | Abu Dhabi – Minimum Room Size** |

|---|---|---|

| 3★ | 15 m² (bathroom included) | 25 m² (single) / 27 m² (double) |

| 4★ | 20 m² (bathroom included) | 30 m² (single) / 32 m² (double) |

| 5★ | 25 m² (bathroom included) | 35 m² (single) / 37 m² (double) |

** Based on the Abu Dhabi Hotel Classification Manual (city property standards).

The room sizes shown are the regulatory minimum thresholds for city hotels. International brand standards and market positioning frequently exceed these minimums.

Why Star Ratings Are Not Spatially Equivalent

While star ratings appear uniform across markets, the quantitative thresholds behind them often differ materially. As demonstrated in the Türkiye vs Abu Dhabi comparison, minimum room sizes, suite ratios, and facility mandates can vary by 20–40% between jurisdictions. A five-star classification in one country may allow room sizes that align with upper-midscale brand standards elsewhere.

For developers, this quantitative variation affects:

- Gross floor area efficiency

- Net-to-gross ratios

- Structural grid design

- Bathroom stacking and plumbing strategy

- Parking allocation

- Land value sensitivity

For example, a 200-room hotel with a regulatory minimum of 25 m² per room requires 5,000 m² of net guestroom area. If the comparable jurisdiction mandates 35 m², that increases to 7,000 m² before corridors, services, and back-of-house. The difference materially impacts capex per key and land absorption efficiency.

A rigorous hotel classification strategy, therefore, requires more than knowing the star level. It requires understanding the underlying spatial metrics and how they interact with brand standards and market ADR expectations.

Market and Operational Classification

Beyond regulation, hotel classification is shaped by market segmentation, property configuration, and operator strategy. Whether a hotel is positioned as luxury, upper upscale, midscale, lifestyle, or extended stay affects spatial planning, service delivery, brand alignment, and revenue strategy. This section explores how hotel classification interacts with property type, operator segmentation, and ownership structure, demonstrating that classification is as much a commercial positioning decision as it is a regulatory designation.

Property Type and Asset Configuration

Hotel classification also reflects asset type. An airport hotel, resort, urban business hotel, boutique property, or extended-stay asset each represents a different operational model embedded within classification.

A resort classification implies higher amenity provision, larger public areas, and greater seasonality risk. An airport classification emphasises efficiency, acoustic insulation, and short-stay turnover. Boutique classification focuses on character and design rather than scale. The classification decision must therefore reflect land value, demand segmentation, and the intended return profile.

Once property configuration is determined, the next strategic layer of hotel classification is operator segmentation, which translates physical format into market positioning, service intensity, and revenue architecture.

Hotel Operator Segmentation Framework

While regulatory hotel classification defines minimum compliance standards, operator segmentation defines how a hotel competes in the market. The framework below outlines common operator segments from economy to luxury, alongside formats such as lifestyle, extended stay, and all-inclusive, and illustrates how positioning influences room-size benchmarks, facility provision, food and beverage strategy, and brand selection.

This segmentation lens is essential for developers, as hotel classification at the operator level directly affects spatial planning, service intensity, capital allocation, and long-term revenue strategy.

| Segment | Typical Room Size (sqm)* | Typical Facilities (Short List) | F&B Strategy | Brand Selection Strategy |

|---|---|---|---|---|

| Economy | 15–20 sqm | Reception, vending, compact lounge | No full restaurant; grab-and-go | Asset-light budget brand, franchise model |

| Midscale | 18–25 sqm | Breakfast room, limited public space | Primarily breakfast; minimal evening offer | Domestic or international economy brand |

| Upper Midscale | 22–30 sqm | Breakfast area, small meeting room, compact gym | Breakfast-focused; limited dinner | Scalable global franchise brand |

| Upscale | 28–38 sqm | Restaurant, bar, fitness room, small meeting space | All-day dining + lobby bar | Recognised international or regional brand |

| Upper Upscale | 32–45 sqm | Full-service restaurant, bar, gym, meeting rooms | Structured full-service with branded F&B | Major international upscale brand |

| Luxury | 40–60+ sqm | Multiple restaurants, spa, concierge, ballroom | Destination-led dining, in-room dining, specialty outlets | Global luxury brand or strong independent |

| Lifestyle / Boutique | 20–35 sqm | Design-led lobby, bar, flexible social space | Experience-driven bar/restaurant | Soft brand or independent concept-driven operator |

| Extended Stay | 25–40 sqm (with kitchenette) | Kitchenette, laundry, small gym, co-working | Minimal F&B; grab-and-go | Extended-stay specialist brand |

| All-Inclusive Resort | 30–50 sqm | Multiple restaurants, pools, spa, entertainment | Multi-outlet, bundled pricing model | International resort-focused brand |

| Select-Service | 20–28 sqm | Breakfast area, compact lobby, limited gym | Breakfast + light evening offer | Franchise-friendly scalable brand |

| Full-Service | 28–45 sqm | Restaurant, bar, meeting rooms, gym | All-day dining + banquet facilities | Global management or franchise brand |

This hotel classification segmentation illustrates how positioning influences spatial standards, facility provision, food and beverage strategy, and brand alignment. As hotel classification moves from economy to luxury, room-size benchmarks typically increase, public space intensity increases, and service delivery becomes more complex.

Brand Influence on Hotel Classification

Global brands apply their own internal hotel classification standards, often exceeding national regulatory minimums. A brand-defined “upper upscale” classification may require room sizes, bathroom layouts, and public space volumes that go well beyond local requirements.

However, classification is not purely linear. Formats such as lifestyle, extended stay, and all-inclusive resorts operate as strategic overlays within the hotel classification spectrum, responding to specific demand patterns rather than traditional star hierarchy. For hotel developers and investors, understanding these distinctions is essential when aligning hotel classification with market feasibility, operator selection, and long-term asset positioning.

Brand alignment influences distribution reach, ADR credibility, loyalty penetration, and eventual liquidity at exit. However, it may also increase capex per key through mandatory design standards and ongoing Property Improvement Plan obligations.

Developers must therefore reconcile three overlapping layers of hotel classification: regulatory classification, brand classification, and market positioning classification.

Franchise vs Management: Classification Implications

Hotel classification is influenced not only by regulatory standards and brand segmentation, but also by the owner’s operating structure. Whether a hotel operates under a franchise agreement or a management contract can materially influence how classification standards are applied and how they are exceeded.

Under a management agreement, the operator typically exercises significant control over design standards, service delivery, staffing models, and brand compliance. As a result, managed luxury and upper upscale hotels often exceed local regulatory minimums, particularly in room size, public space allocation, and service intensity. Operators seek consistency across global portfolios, which can drive higher capital expenditure but also reinforce brand positioning.

Under a franchise structure, the owner retains operational control while adopting brand standards and distribution systems. Franchise models are common in midscale, upper midscale, and select-service segments, where regulatory classification may align more closely with minimum brand thresholds. In such cases, the regulatory star level may represent the lower boundary of compliance rather than an aspirational benchmark.

In emerging markets, the difference becomes more pronounced. A five-star classification achieved through regulatory compliance alone may differ substantially from a five-star branded, managed asset built to international standards. Developers must therefore distinguish between regulatory and operational classifications, particularly when positioning for an institutional exit.

Hotel Classification and Financial Performance

Hotel classification directly influences financial performance across the asset lifecycle. From feasibility modelling and cost-per-key benchmarks to payroll intensity and exit liquidity, classification decisions shape both risk and return. This section examines how hotel classification integrates with valuation methodology, revenue potential, operating cost structure, and investor expectations, reinforcing that classification must align with market demand and long-term capital strategy.

The Integrated Hotel Classification Matrix

Effective hotel classification integrates five core elements: quality level, market segment, property type, regulatory framework, and brand affiliation. These must align with demand forecasts, cost-per-key benchmarks, targeted GOP margins, and anticipated exit yields.

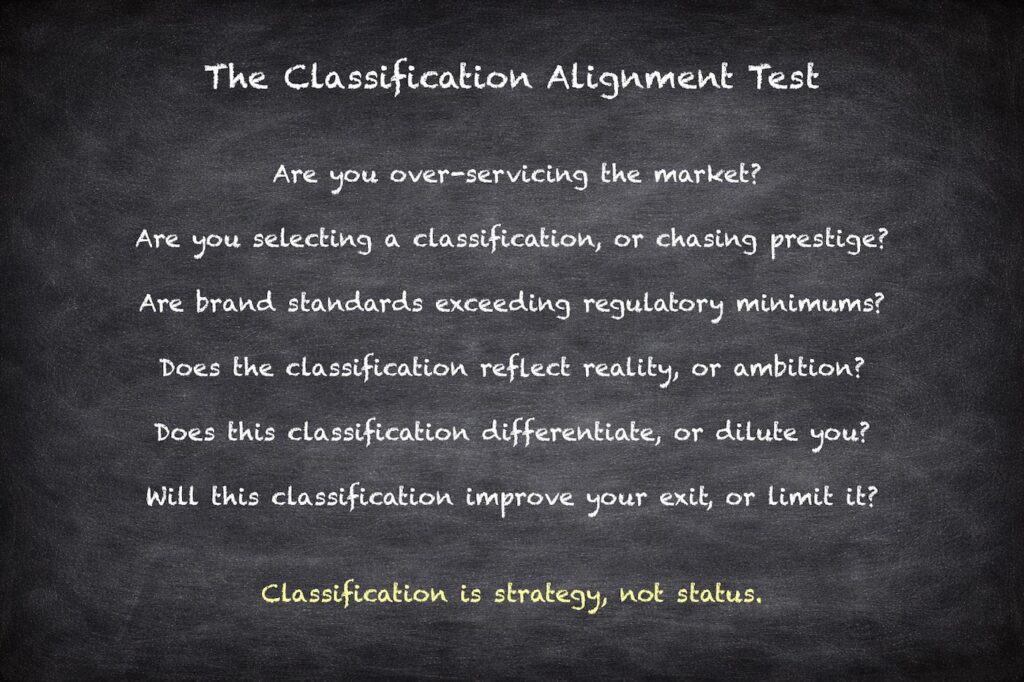

When hotel classification is selected purely for prestige, projects risk becoming overcapitalised relative to their demand base. Conversely, when classification is engineered from feasibility modelling and return objectives, it enhances both operating performance and long-term asset value.

Hotel classification should therefore be tested against three financial questions: What ADR is required to justify land cost? What staffing model is sustainable within projected occupancy? And does the chosen classification align with the likely exit buyer profile?

Financial Alignment and Classification Risk

Incorrect hotel classification is one of the most common root causes of underperformance. Over-classifying a hotel, building to a higher product and service level than the demand base can sustain, compresses return on cost and weakens exit yields.

Under-classifying may limit ADR potential and damage long-term positioning.

Effective hotel classification requires testing the selected standard against projected ADR, occupancy ramp-up, payroll ratios, and stabilisation yields. Classification must support both operational feasibility and exit strategy.

Hotel Classification and Asset Value

Hotel classification directly influences valuation in three primary ways:

1. Revenue Potential

Higher classification can justify higher ADR — but only where demand supports it. If market absorption cannot sustain luxury pricing, over-classification compresses yield.

2. Operating Intensity

Service-heavy classifications increase payroll ratios and fixed cost exposure. While luxury positioning may drive ADR, it can also compress GOP margins if occupancy volatility is high.

3. Exit Liquidity

Institutional investors often prefer branded upper upscale and luxury assets due to perceived stability and brand covenant strength. Conversely, economy and select-service assets may appeal to yield-driven investors seeking operational efficiency.

Importantly, regulatory star level alone does not determine value. Institutional buyers evaluate:

- Brand strength

- Market positioning

- Asset age and PIP exposure

- ESG compliance

- Location fundamentals

- RevPAR index performance

Therefore, hotel classification must be aligned with a long-term exit strategy, not simply development ambition.

Emerging Dimensions of Classification

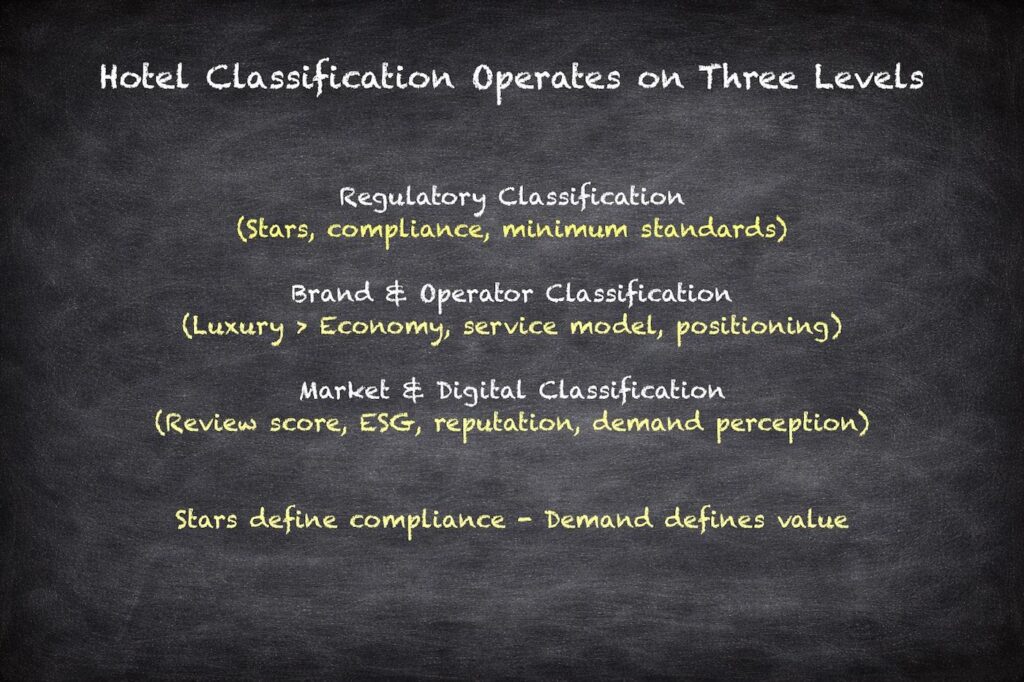

Hotel classification is no longer defined solely by regulatory stars or brand segmentation. Digital reputation systems, sustainability certification, and ESG compliance increasingly overlay traditional classification frameworks, influencing both consumer behaviour and institutional capital flows. This section considers how hotel classification is evolving in response to digital transparency and environmental performance standards, and how developers must incorporate these parallel systems into a forward-looking strategy.

Digital Classification and the Decline of Star Dominance

Traditional hotel classification systems were designed for regulatory clarity and consumer guidance. However, digital platforms increasingly shape market perception more than official stars.

Online Travel Agencies (OTAs), Google Travel, and review platforms influence booking behaviour through:

- Review score (e.g., 8.9 vs 9.3)

- Guest sentiment analytics

- “Preferred Partner” status

- Ranking algorithms

- Review volume and recency

In many markets, a high review score may carry greater commercial weight than a formal five-star designation. As a result, digital classification is emerging as a parallel reputational system that can enhance or undermine regulatory classification.

For investors, this introduces a new dimension: a hotel may hold a five-star regulatory classification yet compete commercially at an upscale level due to digital perception.

ESG and Sustainability as Parallel Classification

Sustainability certifications increasingly overlay traditional hotel classification. Systems such as LEED, BREEAM, Green Key, and national energy-performance frameworks now influence investor appetite and lender requirements.

Unlike star ratings, ESG classification:

- Focuses on carbon intensity and lifecycle efficiency

- Evaluates operational resource management

- Impacts financing costs and institutional eligibility

- Influences exit liquidity

In European markets, alignment with EU Taxonomy principles may increasingly become a quasi-classification layer for institutional assets. For developers, this means hotel classification is no longer only about stars — it also intersects with sustainability positioning and capital market access.

Hotel Classification as a Value Strategy

Hotel classification is not simply a descriptive label; it is a strategic framework that shapes every aspect of a hotel asset’s lifecycle. From concept design and capital budgeting to operational performance and exit valuation, classification decisions influence both risk and return.

For hotel owners and developers, the objective is not to achieve the highest hotel classification possible, but to achieve the most financially aligned classification for the specific market. When hotel classification is integrated into feasibility, valuation modelling, and operator strategy from day one, it becomes a powerful driver of long-term asset performance.

Hotel classification today operates across three parallel systems: regulatory stars, brand segmentation, and digital reputation, increasingly overlaid by sustainability certification. Developers who treat classification as a static label risk misalignment. Those who integrate quantitative standards, digital positioning, ESG compliance, and valuation strategy from inception create assets that are resilient across cycles and jurisdictions.

Further resources:

See HDG – Environmental Design

See HDG – Hotel Asset Management

See HotelStars.eu – “Criteria of the Hotelstars Union“