Hotel valuation sits at the intersection of real estate investment and operating business analysis. Unlike offices, residential blocks, or logistics warehouses, a hotel typically does not generate fixed rental income secured by long leases. Instead, it produces daily trading revenue that fluctuates with demand, pricing power, seasonality, brand strength and management efficiency.

For this reason, hotel valuation requires a deeper analytical approach than most property asset classes. It combines operational literacy, financial modelling, capital markets awareness and strategic timing. Whether acquiring a stabilised asset, refinancing an existing property, developing a new hotel, or planning an exit, understanding valuation mechanics is essential to protecting and enhancing capital.

- The Dual Nature of a Hotel Asset: Real Estate + Operating Business

- The Core Principle: Value Reflects Income Durability and Risk Perception

- The Income Capitalisation Method (Cap Rate Approach)

- EBITDA Multiples and Enterprise Value Perspective

- Discounted Cash Flow (DCF): Forward-Looking Hotel Valuation

- Replacement Cost and Market Equilibrium

- Operational Drivers of Value

- Capital Structure and Cost of Capital in Hotel Valuation

- Hotel Development Valuation and Exit Strategy

- Market Cycles and Timing

- Common Hotel Valuation Mistakes

- Hotel Valuation as Strategic Intelligence

- Hotel Market Analysis & Valuation Software 6.0

The Dual Nature of a Hotel Asset: Real Estate + Operating Business

At its core, a hotel is two assets layered together.

The first layer is real estate: land and building, location, accessibility, physical quality and replacement cost. The second layer is the operating business: revenue management, distribution systems, cost control, brand positioning and guest experience.

Unlike traditional property sectors where income is contractually secured, hotel revenue is variable. Occupancy changes daily. Average Daily Rate (ADR) shifts with demand. Group bookings, corporate contracts and tourism flows can materially influence performance. External shocks, economic downturns, geopolitical events, or travel disruptions can quickly affect trading.

This variability makes risk assessment central to valuation.

In many ownership structures, this duality is formalised through a PropCo / OpCo split (see HDG – Hotel PropCo OpCo Structure). The property company owns the real estate, while the operating company operates the business under a management agreement, franchise agreement, or lease. Each structure reallocates risk differently, and valuation adjusts accordingly.

A lease structure may provide income certainty to the property owner, often compressing cap rates. A management agreement exposes the owner to trading risk but preserves upside. Independent owner-operators carry full volatility but retain maximum control.

Understanding where risk sits within the structure is fundamental before applying any valuation method.

The Core Principle: Value Reflects Income Durability and Risk Perception

All hotel valuation methodologies ultimately reduce to one principle: The value of a hotel reflects the market’s perception of the durability and growth potential of its income stream.

Durable income is derived from diversified demand, strong brand affiliation, efficient management, and prime location, which together command lower yields and higher valuations. Volatile income stemming from seasonal markets, independent positioning, and weak margins attracts higher yields and lower valuations.

Cap rates, EBITDA multiples and discount rates are simply financial expressions of risk perception.

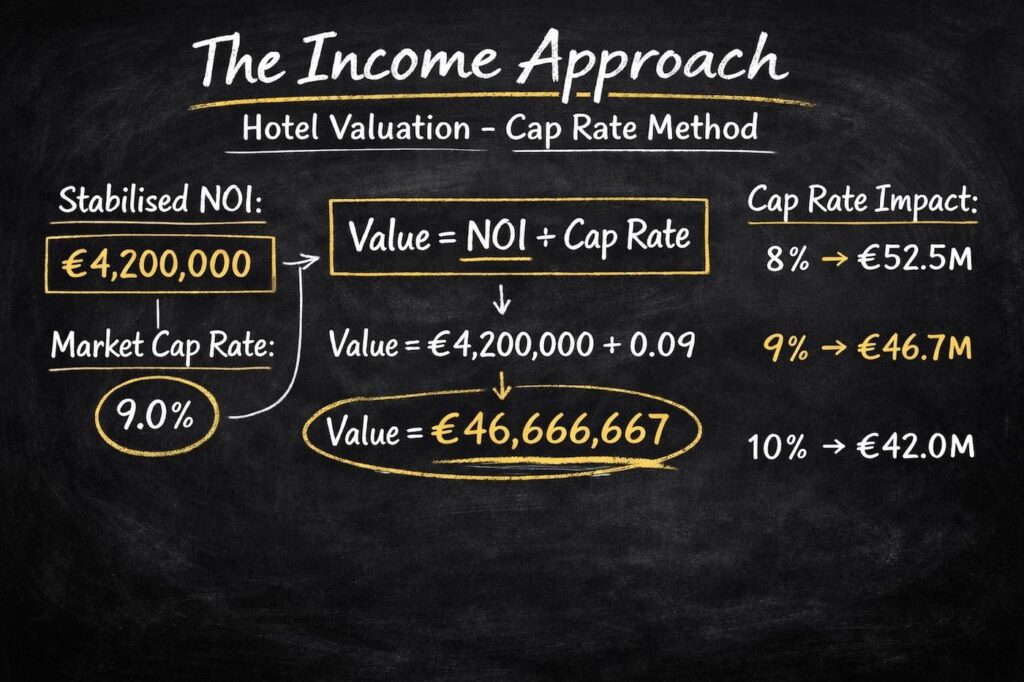

The Income Capitalisation Method (Cap Rate Approach)

The income capitalisation method remains the benchmark reference point in most stabilised hotel transactions. It divides stabilised Net Operating Income (NOI) by a market-derived capitalisation rate.

While the formula is straightforward, the judgement embedded in both inputs determines accuracy.

Establishing Stabilised NOI

NOI must represent sustainable performance rather than peak trading conditions. Buyers and valuers typically adjust for:

- One-off events or temporary demand spikes

- Post-renovation performance distortions

- Unrealistic ADR assumptions

- Under-provisioned operating costs

- Deferred maintenance

Importantly, NOI should reflect realistic FF&E reserve allocations. Hotels require periodic reinvestment to maintain competitive positioning. Failing to account for capital intensity artificially inflates income and overstates value.

Determining the Appropriate Cap Rate for Hotel Valuation

Cap rates are influenced by several variables:

- Market maturity and liquidity

- Economic outlook

- Brand covenant strength

- Management structure

- Asset age and quality

- Investor competition

Prime gateway city hotels with global brands may transact at materially lower cap rates than independent secondary-market properties. During expansion phases, yield compression occurs as capital competes for limited product. During downturns, cap rates expand to compensate for perceived volatility.

The sensitivity of value to yield movement is substantial. A hotel generating €5 million in stabilised NOI valued at an 8% cap rate produces a €62.5 million valuation. If yields move to 9%, value falls to €55.6 million. At 10%, value declines to €50 million.

Yield movement alone can create significant equity volatility even when operational performance remains constant.

EBITDA Multiples and Enterprise Value Perspective

In institutional transactions and portfolio sales, valuation discussions often reference EBITDA multiples rather than cap rates. This approach frames the hotel more explicitly as a trading business.

Enterprise value is calculated as EBITDA multiplied by a market multiple. The multiple reflects expected growth, stability and exit liquidity.

Hotels affiliated with international operators such as Marriott International, Hilton or Accor often achieve stronger distribution and loyalty support, enhancing revenue stability. This may justify higher EBITDA multiples compared to independent properties.

However, brand affiliation is not purely additive. Management and franchise fees reduce net profitability. Performance clauses, incentive fee structures and termination provisions must be analysed carefully.

The EBITDA multiple approach is particularly useful when evaluating portfolios where capital structure, synergies and cost efficiencies influence value beyond single-asset metrics.

Discounted Cash Flow (DCF): Forward-Looking Hotel Valuation

The Discounted Cash Flow method provides a forward-looking valuation framework. Rather than capitalising a single year of income, it projects multi-year performance and discounts future cash flows back to present value.

DCF is particularly relevant in development, repositioning or turnaround scenarios where current performance does not reflect long-term potential.

Key components include:

- Revenue projections based on occupancy and ADR growth

- Margin stabilisation assumptions

- Capital expenditure cycles

- Terminal value derived from an assumed exit cap rate

- Discount rate reflecting required return

Small changes in exit cap rate assumptions can materially affect IRR outcomes. For developers, modelling conservative exit yields is essential to protect downside risk.

While DCF provides analytical depth, its reliability depends entirely on the realism of assumptions. Over-optimistic growth modelling remains one of the most common valuation errors in development feasibility studies.

Replacement Cost and Market Equilibrium

Replacement cost analysis provides a useful contextual benchmark. It calculates what it would cost to build the same hotel today, including land, construction, professional fees, financing, pre-opening expenses and FF&E.

When transaction values exceed replacement cost by significant margins, development activity accelerates. When market values fall below replacement cost, new supply slows.

Monitoring the relationship between income-based valuation and replacement cost offers insight into cycle positioning and development feasibility.

Replacement cost does not directly determine market value, but it defines economic boundaries for rational investment.

Operational Drivers of Value

Beyond financial modelling, several operational factors materially influence valuation.

Location and Demand Diversity

Hotels located in diversified demand markets, combining corporate, leisure, group, and international segments, typically achieve more stable performance. Assets that are heavily reliant on a single demand driver exhibit higher volatility and, therefore, higher cap rates.

Proximity to transport nodes, convention centres, financial districts and tourist attractions enhances demand resilience.

Brand Strength and Distribution

Global distribution platforms, loyalty programmes and corporate sales networks support occupancy stability. International operators such as Marriott International and Hilton reduce perceived demand risk in the eyes of many investors.

However, independent boutique hotels can command premium valuations if margins are superior and positioning is strong. Brand is a risk mitigator, not a guarantee of value.

Management Structure and Contract Terms

The specific terms of management or franchise agreements materially affect valuation. Base fees, incentive fees, key money provisions, performance tests and termination rights all influence risk allocation.

Lease structures often attract lower cap rates due to income certainty, but lease covenant quality is critical. A weak tenant does not justify yield compression.

Margin Discipline

High GOP and EBITDA margins signal operational efficiency. Investors scrutinise departmental profit ratios, payroll structure, energy costs and distribution channel mix.

Strong margin discipline enhances income durability and may justify premium pricing.

Capital Structure and Cost of Capital in Hotel Valuation

Hotel valuation cannot be separated from capital structure. The weighted average cost of capital influences required returns and discount rates.

Assets financed with high leverage may achieve attractive equity IRRs but face refinancing risk if values decline. Lenders typically apply conservative Loan-to-Value ratios for hotels due to income volatility.

Banks and credit funds analyse debt service coverage ratios, stress-test occupancy assumptions, and require independent valuations from firms such as HVS, CBRE, JLL, and Knight Frank.

Understanding lender underwriting methodology allows sponsors to anticipate valuation constraints before entering financing negotiations.

Hotel Development Valuation and Exit Strategy

For developers, the central valuation question is forward-looking: “What will the hotel be worth once stabilised?“

Development feasibility models typically project a two- to four-year ramp-up period followed by stabilised EBITDA. The projected exit value is calculated by applying an assumed cap rate to stabilised income.

Land value is often derived residually after satisfying required IRR thresholds. If projected exit value does not exceed total development cost plus target return, the scheme is economically unviable.

Yield assumptions are critical. Modelling a 7.5% exit cap rate rather than 8.5% can transform apparent profitability. Conservative underwriting is essential to protect against cycle shifts.

Professional developers routinely run multiple sensitivity scenarios to test downside resilience.

Market Cycles and Timing

Hotels are among the most cyclical real estate assets. During periods of economic expansion and strong travel demand, income growth accelerates and cap rates compress. In downturns, occupancy declines rapidly and yields expand.

Strategic timing can create significant value independent of operational improvement. Acquiring during yield expansion and exiting during compression can materially enhance returns.

Understanding macroeconomic indicators, capital market liquidity and investor sentiment is therefore integral to valuation strategy.

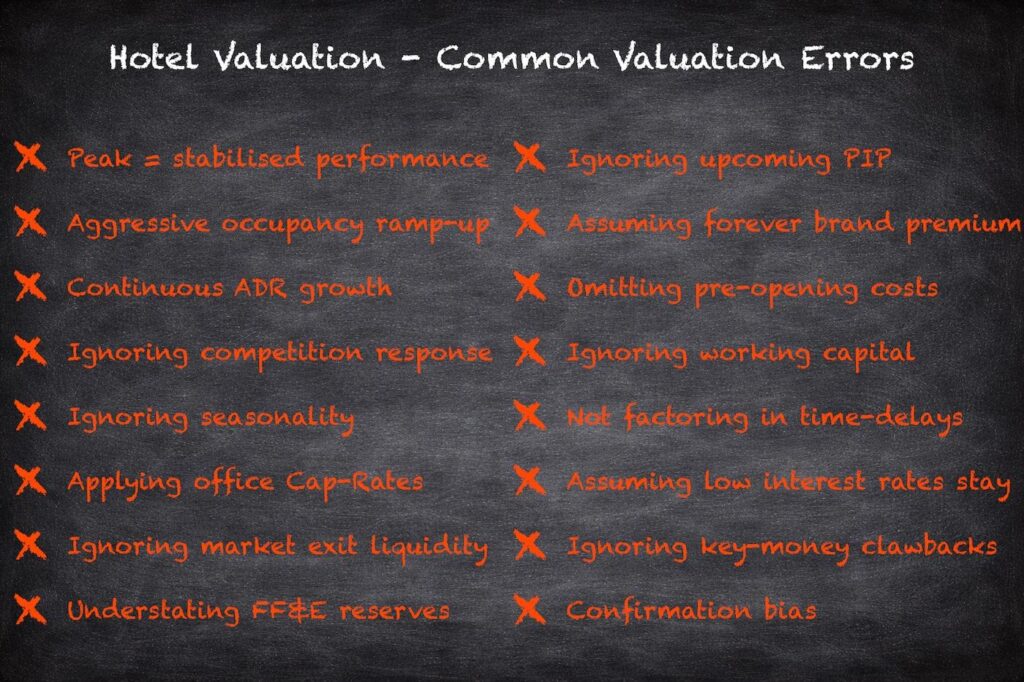

Common Hotel Valuation Mistakes

Valuation errors frequently stem from misunderstanding volatility. Applying office-sector cap rates to hotel assets understates risk. Ignoring FF&E cycles inflates sustainable income. Overestimating ADR growth or occupancy stabilisation creates unrealistic projections.

Another frequent mistake is neglecting management agreement obligations, including incentive fee thresholds or brand-mandated capital expenditure.

Disciplined underwriting and conservative assumptions remain the foundation of credible hotel valuation.

Hotel Valuation as Strategic Intelligence

Hotel valuation is not a mechanical formula. It is a strategic assessment of income durability, operational competence, structural risk and market timing.

Investors who understand valuation drivers gain competitive advantage in acquisition pricing, refinancing negotiations, development feasibility and exit planning.

Ultimately, value reflects confidence in future income. The more durable and resilient that income appears, the stronger the valuation.

Hotel Market Analysis & Valuation Software 6.0

eCornell Education Website / Hotel Valuation Software Website

One of the most recognised structured tools in professional hotel appraisal is Hotel Market Analysis & Valuation Software 6.0, developed by Steve Rushmore, founder of HVS, and Jan deRoos. The software was designed to formalise the methodology behind hotel market studies, financial forecasting and valuation assignments. Delivered as an Excel-based platform (Windows and macOS compatible), it provides a transparent, non-proprietary modelling framework tailored to the hospitality sector, rather than adapting generic real estate templates.

The system consists of three integrated models. The Hotel Market Analysis and ADR Forecasting Model quantifies competitive supply, segments demand, and projects ten-year occupancy and average daily rate using a proprietary competitive-indexing algorithm. The Hotel Revenue and Expense Forecasting Model converts these projections into detailed 11-year financial statements aligned with the Uniform System of Accounts for Hotels, modelling how revenues and costs evolve as occupancy and ADR increase. Finally, the Hotel Mortgage-Equity Valuation Model incorporates real-world financing assumptions, including loan-to-value ratios, debt service coverage and equity return requirements, to calculate value based on blended capital structures rather than relying solely on simplified discounted cash flow techniques.

In practice, the software allows consultants, lenders, owners and developers to move systematically from market analysis through financial projection to leveraged valuation, making it particularly useful for feasibility studies, refinancing analysis, capital expenditure evaluation and development exit modelling. While it requires methodological discipline to use effectively, structured training and certification programmes are available through its developer. For investors and developers seeking a defensible, hospitality-specific analytical framework, the platform provides a rigorous bridge between operational forecasting and capital market valuation.

Further resources:

See HDG – Hotel Asset Management

See HDG – Hotel Owning Structure

eCornell – “Valuing Hotel Investments Through Effective Forecasting” Cornell Educational Course

hotelvaluationsoftware.com – Download a Free Copy of the Software Manual and Case Study