Hotel asset management exit strategies form a critical component of the hotel investment lifecycle, shaping how value is created, protected, and ultimately realised. Whether the objective is a stabilised hotel asset sale, a sale-and-leaseback, a portfolio disposal, or a strategic divestment under a PropCo–OpCo structure, exit planning directly influences capital expenditure decisions, operator selection, brand alignment, and financing structure.

- Exit Strategy Is Engineered from Day One

- Defining the Target Buyer: Who Are You Building This Asset For?

- Core Hotel Exit Routes in Asset Management

- Timing the Exit: Market Cycle Considerations

- Preparing for Exit: A Three-Year Asset Management Roadmap

- Valuation Mechanics at Exit

- Common Hotel Exit Strategy Mistakes

- Tax and Structuring Considerations

- Exit Strategy Within the PropCo–OpCo Model

- Exit Strategy as a Continuous Discipline

Exit Strategy Is Engineered from Day One

Hotel asset management exit strategies are not made at the last minute when a broker is appointed; they are engineered from the acquisition or development stage. Sophisticated hotel investors underwrite their exit on day one because the expected disposal route influences brand selection, operator structure, capital expenditure timing, debt strategy, and even the building’s physical specifications. In other words, exit planning is a value creation discipline, not a disposal event.

In hotel real estate, value is a function of stabilised net operating income (NOI), perceived risk, and capital market conditions. Asset managers are responsible for shaping all three. They influence NOI through operational oversight and capital planning. They influence risk perception through contract structuring, brand alignment, and governance. And while they cannot control macroeconomic cycles, they can prepare an asset to perform optimally within them. A structured hotel investment exit strategy, therefore, sits at the core of professional asset management, not at its periphery.

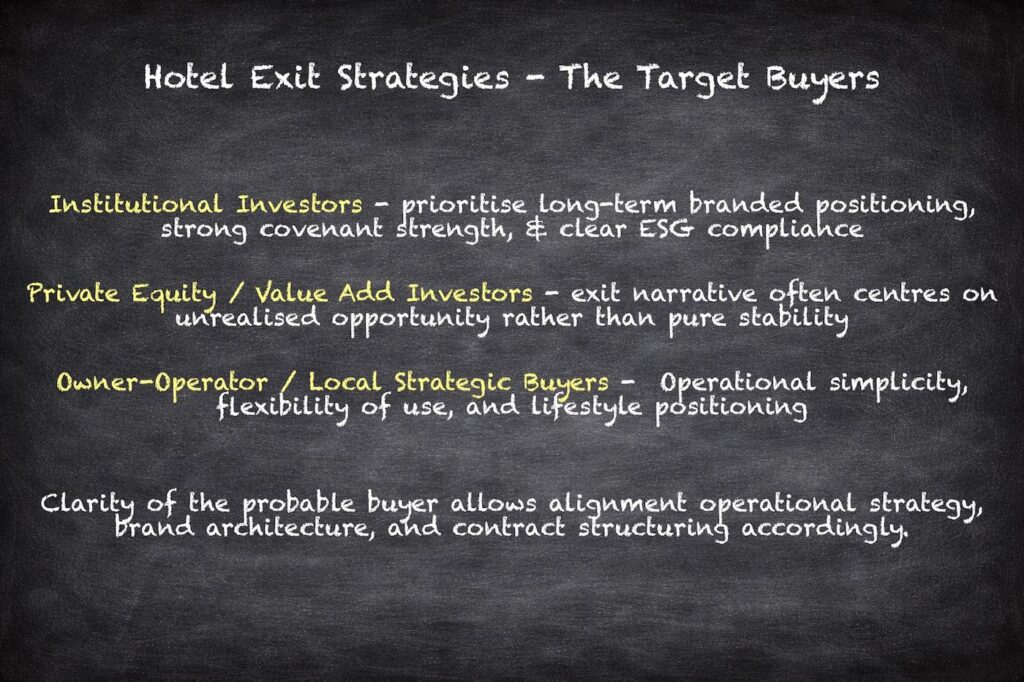

Defining the Target Buyer: Who Are You Building This Asset For?

Every hotel asset management exit strategy should begin with a clearly defined buyer universe. A hotel that appeals to an institutional core fund is not structured in the same way as one targeting a private equity value-add investor or a local owner-operator. Failure to define the end buyer often results in misaligned contracts, suboptimal brand positioning, or capital structures that deter potential acquirers.

Institutional Investor Exit

Institutional investors seek stable, predictable cash flows with minimal operational volatility. These buyers typically prioritise long-term branded positioning, strong covenant strength, and clear ESG compliance. For this buyer profile, the asset manager’s focus in the years preceding exit is on:

- Stabilising NOI and reducing earnings volatility

- Ensuring long-term management or lease agreements are market-standard and assignable

- Delivering clean, auditable financial reporting

- Demonstrating resilience across market cycles

Institutional buyers price risk conservatively. A hotel operating under a globally recognised brand with a transparent fee structure and robust governance framework will typically command a lower cap rate than an equivalent independent asset with opaque reporting.

Private Equity or Value-Add Buyer

Value-add investors look for repositioning potential. They may accept operational volatility if there is clear upside in ADR, occupancy, brand conversion, or capital-expenditure efficiency. For this buyer profile, the exit narrative often centres on unrealised opportunity rather than pure stability.

Asset managers preparing for this exit route may intentionally retain some repositioning scope, such as:

- Brand conversion potential

- Underutilised F&B or event space

- Revenue management inefficiencies

- Expansion or extension rights

In these cases, value is framed not only through trailing performance but also through forward-looking business plans supported by credible market data.

Owner-Operator or Local Strategic Buyer

Smaller assets, secondary city hotels, or boutique lifestyle properties may appeal more to local buyers or owner-operators. These buyers often require higher yields and are more comfortable with operational exposure. The exit strategy here may focus less on institutional-grade governance and more on operational simplicity, flexibility of use, and lifestyle positioning.

Clarity regarding the intended buyer universe allows the asset manager to align operational strategy, brand architecture, and contract structuring accordingly.

Core Hotel Exit Routes in Asset Management

A structured hotel exit strategy recognises that disposal can occur through multiple mechanisms. Each route carries different pricing dynamics, risk allocations, and capital implications.

Sale of a Stabilised Asset

The most traditional hotel investment exit involves selling the asset based on stabilised NOI divided by an appropriate market cap rate. However, “stabilised” must be clearly defined. Buyers will scrutinise trailing twelve-month (TTM) performance, normalised expenses, capital reserves, and sustainability of earnings.

Asset managers typically begin preparing for this route 24 to 36 months in advance. This preparation includes:

- Eliminating non-recurring owner expenses

- Addressing deferred maintenance

- Ensuring capex aligns with brand standards

- Optimising GOP margins without artificially suppressing necessary reinvestment

Cap rate sensitivity can significantly impact value. A 25-basis-point shift in exit yield can materially affect pricing, particularly for larger assets. Therefore, positioning the asset to appeal to the broadest possible buyer base reduces yield volatility risk.

Forward Sale or Forward Funding

In development-led strategies, exit may occur before stabilisation through forward sale or forward funding arrangements. These structures reduce development risk and allow capital recycling at an earlier stage, though typically at a lower return compared to full stabilisation.

Asset managers involved in development projects must ensure that brand, specification, and contract structures align with institutional acquisition criteria from inception. A forward sale buyer will underwrite completion risk, operator covenant, and delivery quality, meaning exit considerations must inform design decisions long before construction concludes.

Sale and Leaseback

Sale and leaseback structures allow an owner to monetise the real estate (PropCo) while retaining operational control through the OpCo under a long-term lease. This approach can unlock capital while preserving operational upside.

However, over-renting the asset in pursuit of higher valuation multiples can introduce long-term covenant stress. Rental coverage ratios, lease indexation terms, and covenant strength must be carefully modelled to ensure sustainability. Asset managers must balance short-term valuation optimisation against long-term financial resilience.

Conversion or Alternative Use Exit

In certain markets, highest and best use may not remain hotel. Urban assets in prime locations may achieve greater value through residential, student housing, co-living, or office conversion. Asset managers should periodically conduct highest-and-best-use analyses, particularly when hotel performance lags broader real estate appreciation.

This strategy requires careful review of zoning, planning permissions, and structural feasibility. Exit timing may hinge on regulatory windows or local market dynamics rather than purely operational performance.

Portfolio Exit Strategy

Aggregating multiple assets into a portfolio can generate pricing premiums due to scale, geographic diversification, and platform value. Portfolio exits often attract institutional capital seeking deployment efficiency.

Standardised reporting, centralised governance, and harmonised contract structures become critical in these scenarios. A portfolio strategy is not simply the sum of individual asset exits; it requires coordinated preparation and consistent asset management discipline across properties.

Timing the Exit: Market Cycle Considerations

Hotel asset management exit strategies must account for capital market cycles. Selling during peak RevPAR does not always equate to selling at peak valuation. Buyers underwrite future earnings, not just historical performance.

Interest rate environments materially influence cap rates. Rising rates can expand yields, compressing values even in stable operational environments. Conversely, periods of yield compression can amplify pricing, particularly for core, stabilised assets.

Asset managers must monitor:

- Debt market liquidity

- Inflation expectations

- Tourism demand fundamentals

- Regulatory shifts

- Geopolitical considerations

In emerging or tourism-dependent markets, currency exposure and policy stability can materially affect buyer appetite. Strategic timing, therefore, requires macro awareness alongside operational excellence.

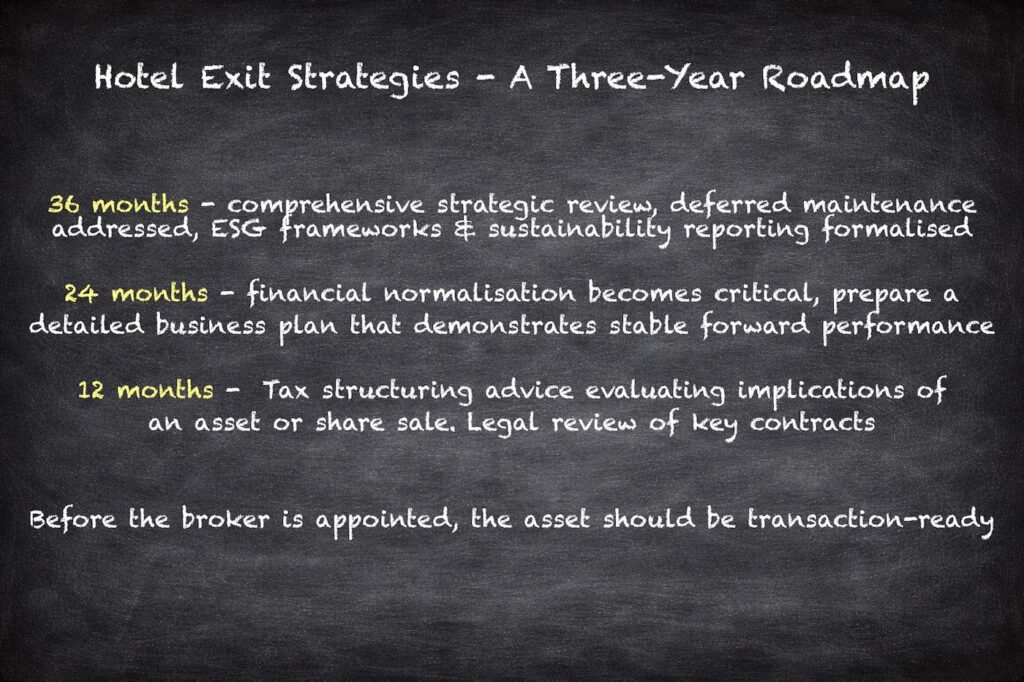

Preparing for Exit: A Three-Year Asset Management Roadmap

Professional hotel exit strategies are executed over a multi-year horizon. The following phased approach illustrates how asset management integrates exit preparation into operational planning.

36 Months Before Exit

Three years prior to disposal, the asset manager should conduct a comprehensive strategic review. This includes evaluating brand competitiveness, management agreement flexibility, capital expenditure backlog, and market positioning.

Deferred maintenance must be addressed early to avoid last-minute capital spikes. ESG frameworks and sustainability reporting should be formalised, as institutional buyers increasingly scrutinise environmental performance and regulatory compliance.

At this stage, the focus is on structural and strategic matters rather than on transactional matters.

24 Months Before Exit

Two years out, financial normalisation becomes critical. Owner-specific expenses should be clearly separated from operational costs. Staffing levels should reflect sustainable operations rather than temporary optimisation.

The asset manager should prepare a detailed business plan that demonstrates stable forward performance. Market benchmarking data, competitor analysis, and revenue management validation strengthen the sales narrative.

Preliminary valuation advice may be commissioned to test assumptions and refine strategy.

12 Months Before Exit

Within the final year, attention shifts to transaction readiness. A data room should be prepared, containing audited financials, management agreements, lease documentation, brand contracts, technical reports, and compliance certificates.

Trailing twelve-month performance should reflect stability rather than volatility. Tax structuring advice should be sought to evaluate the implications of an asset sale versus a share sale. Legal review of assignment clauses, termination rights, and key contracts reduces execution risk during negotiations.

By the time the broker is appointed, the asset should already be transaction-ready.

Valuation Mechanics at Exit

Understanding valuation dynamics is fundamental to hotel asset management exit strategies. In simplified terms:

Value = Stabilised NOI ÷ Exit Cap Rate

However, both components are heavily scrutinised. Buyers adjust NOI for sustainable performance, reserve provisions, and capital expenditure requirements. Exit cap rates reflect perceived risk, contract structure, brand strength, and macroeconomic conditions.

Factors influencing exit valuation include:

- Remaining term of management or lease agreements

- Brand recognition and covenant strength

- Market depth and liquidity

- Asset quality and capital expenditure history

- Land tenure structure (freehold vs leasehold)

Even minor yield movements can create substantial value fluctuations. Sensitivity analysis should form part of every asset manager’s exit modelling process.

Explore HDG – Hotel Valuation | A Guide to Cap Rates, EBITDA, DCF & Development Exit Value →

Common Hotel Exit Strategy Mistakes

Despite increasing sophistication in hotel asset management, recurring mistakes undermine exit value.

- Overestimating cap rate compression is a frequent error. Assuming that future market conditions will justify lower yields can lead to unrealistic pricing expectations and delayed transactions.

- Selling before genuine stabilisation is another common misstep. Buyers discount volatility aggressively. A consistent performance track record often yields better pricing than a short-lived performance spike.

- Failing to align with the buyer universe can also reduce value. Signing overly restrictive management agreements, failing to ensure assignability, or neglecting covenant strength may deter institutional capital.

- Finally, inadequate data room preparation slows transactions and erodes buyer confidence. Transparency and organisation materially influence pricing and negotiation leverage.

Tax and Structuring Considerations

Tax structuring can materially affect net exit proceeds. Asset sale versus share sale structures carry different capital gains and VAT implications depending on jurisdiction. Corporate tax timing, loss utilisation, and withholding considerations must be evaluated in advance.

In some cases, REIT conversion or restructuring may enhance liquidity and investor appeal. Cross-border investors must consider repatriation rules, double taxation treaties, and currency exposure.

Asset managers are not tax advisers, but proactive coordination with legal and tax professionals ensures that exit structuring aligns with broader investment objectives.

Exit Strategy Within the PropCo–OpCo Model

Where a hotel operates under a PropCo–OpCo structure, exit complexity increases. Investors may dispose of:

- PropCo only (retaining operational interest)

- OpCo only (retaining real estate ownership)

- Both entities simultaneously

Assignment clauses, termination rights, and management agreement flexibility become central to transaction feasibility. Lease structures may enhance income visibility but can also constrain pricing if rental levels are unsustainable.

Asset managers must understand how structural separation affects buyer appetite and valuation metrics.

Explore HDG Hotel PropCo / OpCo Structure Explained →

Exit Strategy as a Continuous Discipline

Hotel asset management exit strategies are most successful when treated as continuous disciplines rather than isolated events. Every operational decision, brand alignment choice, capital expenditure programme, and contractual negotiation influences future liquidity.

The strongest exits are prepared years in advance, supported by transparent reporting, disciplined governance, and a clearly defined buyer universe. In an asset class characterised by operational complexity and capital intensity, structured exit planning protects value, enhances pricing resilience, and maximises investor returns.

For owners, developers, and investors seeking to optimise hotel value across the full investment lifecycle, exit strategy and asset management must operate as a single, integrated framework.

Further resources:

See HDG – Hotel Asset Management

See HDG – Hotel Valuation | A Guide to Cap Rates, EBITDA, DCF & Development Exit Value

See HDG – Hotel PropCo / OpCo Structure Explained

Hotel Management Magazine – “Mastering the art of hotel investment: Crafting an exit strategy” January 2024